AI Voice Agents for Lenders: 7 Use Cases | Fortay Connect

by

Fortay Connect

|

25th Jun 2026

Posts By Topics

- AI (18)

- News (17)

- Unified Communications (17)

- Contact Centre (16)

- Ring Central (13)

- Zoom (13)

- CX (12)

- Events (12)

- Virtual Agent (9)

- Avaya (7)

- Financial Services (7)

- GoToConnect (7)

- Contact Centre Consulting (6)

- Partners (6)

- Case Studies (5)

- Resources (5)

- Unified Communications Solutions (5)

- AI Meeting Assistant (2)

- AI Sales Analytics (2)

- Chatbot (2)

- Conversational Intelligence (2)

- Employee Communications (2)

- Legal (2)

- Microsoft Teams (2)

- Trends (2)

- Video (2)

- AI Companion (1)

- AI Receptionist (1)

- DialPad (1)

- Neurodiversity (1)

- Omnichannel (1)

- Sentiment Analysis (1)

- workvivo (1)

AI Voice Agents for Lenders: 7 Use Cases | Fortay Connect

25 June 2026

AI Voice Agents for Lenders: Where They Actually Pay Off, From Servicing to Arrears

AI voice agents work in lending. But only when they are pointed at the right calls.

The strongest commercial returns come from high-volume, low-judgement interactions: routine servicing queries, payment reminders, balance and settlement enquiries, and early-stage arrears outreach. Complex forbearance conversations, customers showing signs of financial difficulty, complaints and disputed balances all stay with human specialists. That boundary is not a compliance footnote; it is the commercial logic of the whole model.

The correct frame for ROI is not headcount reduction. It is freed agent capacity, faster first contact, better out-of-hours coverage, and higher throughput on routine work so your specialist teams can focus on the calls that genuinely require human judgement.

Key takeaways

- AI voice agents pay off first in high-volume, repeatable servicing and routine arrears interactions, not in complex hardship or dispute handling.

- The FCA's Financial Lives 2024 survey found that 52% of UK adults show at least one characteristic of vulnerability, which makes explicit escalation design non-negotiable, not optional.

- The commercial gain is faster coverage and freed specialist capacity, not indiscriminate cost-cutting.

- Start narrow: one bounded call type with clean escalation rules, then expand once controls are proven.

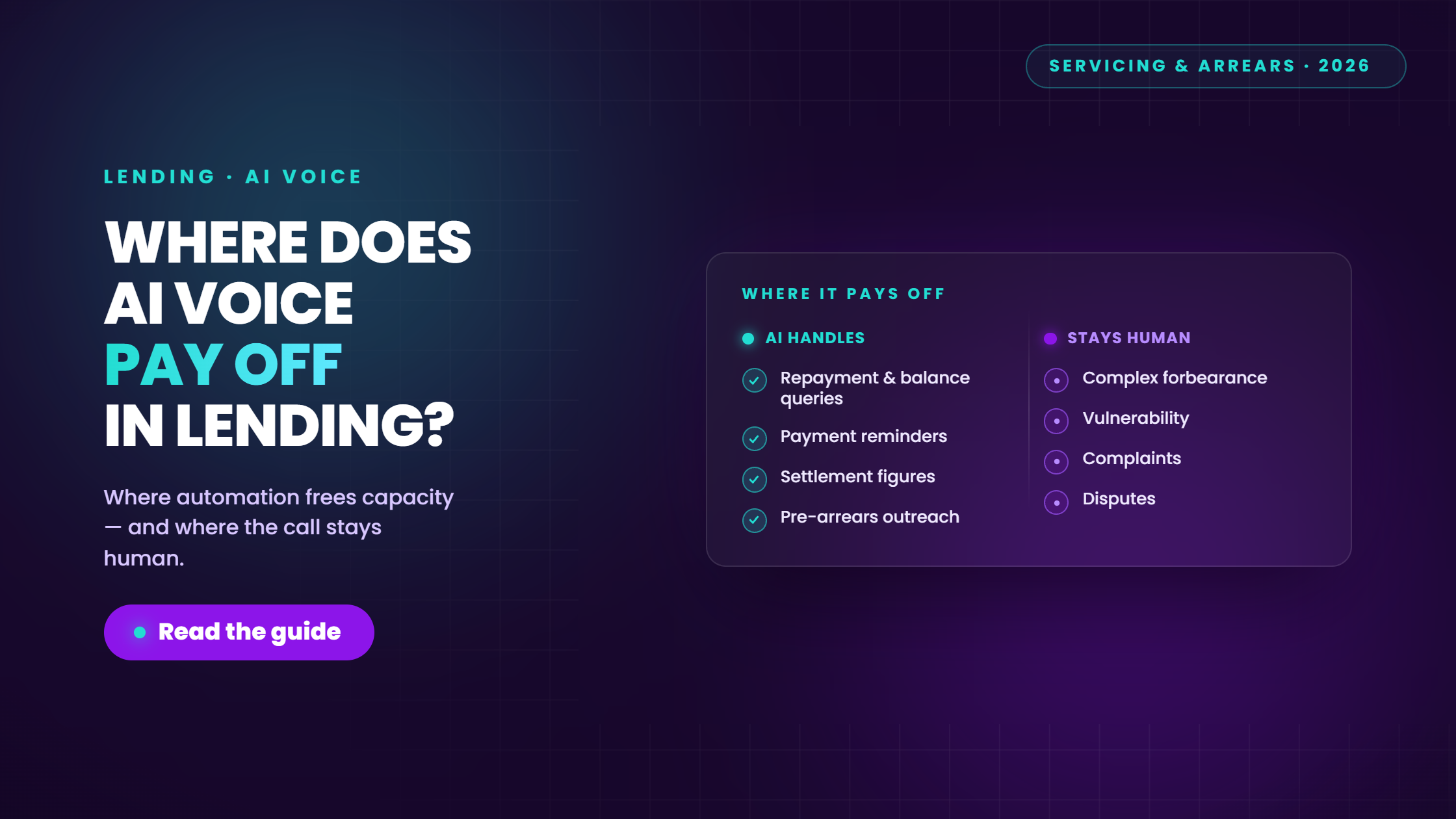

Which lending calls actually pay off to automate?

The practical filter is three questions: Is this call high volume? Is the outcome predictable from the information the customer provides? Does it require agent discretion beyond following a deterministic policy rule? If the answer to the first two is yes and the third is no, it is a strong candidate.

The table below maps the split for most lending operations.

|

Good first AI voice use cases |

Keep human-led |

|---|---|

|

Repayment date and amount queries |

Complex affordability conversations |

|

Outstanding balance and settlement figure requests |

Customers showing signs of financial difficulty or vulnerability |

|

Payment confirmation and receipt queries |

Nuanced forbearance and hardship arrangements |

|

Application and decisioning status checks |

Complaints and disputed balances |

|

Standard ID and verification steps |

Litigation-related matters |

|

Simple payment arrangement setup (policy-driven) |

Any call where the customer deviates from the expected path |

|

Pre-arrears payment reminders and outreach |

Complex repossession or enforcement discussions |

|

Standard product and rate change notifications |

Customers requiring mental health or financial wellbeing support |

The borderline calls

Some interactions sit in the middle. A payment reminder that starts routine can quickly surface genuine financial difficulty. A settlement enquiry can become a complaint. The right design is not to categorise these as either safe or unsafe in advance; it is to build the AI to detect deviation early and hand off cleanly.

The practical rule: if the agent handling this call would need to exercise discretion, apply policy judgement, or make a decision that affects a customer's financial position in a meaningful way, it should not be contained by AI. The moment the call requires anything beyond retrieving information or confirming a deterministic policy outcome, escalation should be immediate and seamless.

A motor finance lender we worked with drew this boundary clearly: AI took routine repayment queries and simple arrangement confirmations; specialist agents handled everything involving changed circumstances or hardship. That split, not the technology itself, was what made the business case defensible.

What is the cost and ROI case?

The economics of AI voice in lending rest on a simple principle: routine conversations handled at a lower marginal cost, with coverage extended beyond staffed hours, free your specialist agents to work higher-value interactions.

Indicative figures in the market suggest AI voice can handle routine calls at somewhere in the region of 20p to 30p per minute, compared with five to eight times that for a fully loaded live agent minute. Treat those numbers as directional; actual cost depends on telephony infrastructure, orchestration layer, integration complexity, and how your escalation model is designed. Any vendor quoting a single universal rate should be pressed for a full total cost of ownership model before you build a business case around it.

McKinsey's research on digital-first collections found that well-designed programmes can reduce collections costs by at least 15%, with stronger resolution and repayment performance than traditional approaches. The mechanism is the same as the voice agent model: move lower-complexity work to lower-cost channels, and free specialist capacity for the interactions that need it.

The real ROI frame The gain is not just lower cost per contact. It is:

- More attempts worked in the same staffed period

- Faster time to first contact on early-stage arrears (one mortgage servicer reduced first contact from over six days to just over one day with automated outreach)

- Higher containment on routine servicing, which reduces queue pressure for specialist agents

- Arrangement throughput that does not depend on staffing levels or shift patterns

What to measure

Vanity metrics like deflection rate look good in a board deck but tell you little about commercial value. The measures that matter for a lending business case are:

- Freed specialist capacity (hours recovered for complex case handling)

- Cost per resolved routine interaction (not blended cost per call)

- Time to first contact on early-stage arrears and pre-arrears outreach

- Arrangement completion rate on AI-handled simple setups

- Escalation quality (are handoffs happening at the right point, with full context passed to the agent?)

If your pilot cannot move at least two of these metrics meaningfully, the scope is probably too narrow or the integration too shallow to demonstrate real value.

Can AI handle collections and arrears calls?

Yes, within clearly defined boundaries. This is the section most lenders approach with the most caution, and rightly so. Arrears and collections calls touch customers who may be financially stressed, vulnerable, or both. The answer is not to avoid automation here; it is to be precise about which part of the arrears journey AI can handle responsibly.

What AI can handle in arrears

The following interactions are well suited to AI voice when escalation rules are explicit and tested:

- Pre-arrears outreach - proactive reminders ahead of a missed payment, with an easy path to speak to an agent if the customer indicates difficulty

- Simple promise-to-pay capture - confirming a payment date and amount where no policy exception or affordability discussion is required

- Standard arrangement setup - where the terms are policy-driven and the customer's circumstances are straightforward

- Payment confirmation and receipt - confirming a payment has been received and updating the customer on their account status

- Early-stage arrears status queries - balance, arrears amount, next steps, where no dispute or hardship is indicated

What must escalate immediately

- Any indication of financial difficulty, distress, or changed circumstances

- Customers who mention job loss, illness, bereavement, or relationship breakdown

- Any sign of vulnerability, including confusion, distress, or difficulty engaging with the process

- Complaints or expressions of dissatisfaction with how the account has been handled

- Disputed balances or disagreements about what is owed

- Any request for a payment holiday, reduced payment, or other forbearance arrangement that requires judgement

The escalation design is not optional. It is the mechanism that keeps AI deployment in arrears commercially viable and operationally responsible. For the full governance framework on vulnerable customer handling and Consumer Duty obligations in automated servicing, see our Consumer Duty guide for contact centres and our FCA voice agent compliance overview.

The boundary between routine and complex is where most implementations succeed or fail. A well-designed handoff, with full conversation context passed to the specialist, is worth more than any efficiency gain from containment.

What about self-service across channels?

Voice is where most lending automation starts, but the strongest operational gains come when routine servicing works coherently across channels. Customers do not stay in one channel: they might receive an SMS reminder, click through to a web journey, and then call to confirm. If those touchpoints are disconnected, the customer restarts the interaction each time and your agents absorb the duplication.

A mortgage servicer we worked with was running collections outreach across phone, SMS, and web with no shared context between them. Customers were being contacted multiple times on the same matter through different channels, with no visibility across the operation. Consolidating onto a coordinated platform reduced duplicate handling and gave the collections team a single audit trail across all touchpoints.

- Voice handles inbound servicing queries and outbound payment reminders

- SMS drives pre-arrears outreach and appointment confirmation at lower cost per contact

- WhatsApp supports document exchange and two-way servicing for customers who prefer messaging

- Web self-service covers balance checks, payment scheduling, and settlement requests without agent involvement

The operational benefit is not just efficiency. A single platform view improves outcome coding, escalation handoff, and the audit trail regulators expect. It also makes it easier to identify customers who are cycling through multiple channels without resolving their query, which is often an early indicator of difficulty.

For guidance on platform selection across these channels, see our AI virtual agent vs chatbot comparison.

What about out-of-hours and overflow?

For many lending teams, the fastest ROI is not replacing daytime agents. It is capturing the contact volume that currently falls through the gaps.

Customers do not arrange their financial concerns around your staffed hours. A missed call at 8pm on a payment query can become a missed arrangement, an escalated arrears case, or a complaint. AI voice can hold that contact window open without the cost of extended shift cover.

Where out-of-hours and overflow coverage pays off:

- Month-end cycles - predictable spikes in payment queries and arrangement requests that would otherwise queue into the following morning

- Rate change events - mortgage and consumer lending rate changes generate high inbound volumes in short windows; AI absorbs the routine enquiries while specialist agents handle the complex ones

- Campaign-driven surges - outbound collections campaigns create inbound callbacks that are difficult to staff for without temporary headcount

- After-hours servicing - balance checks, settlement requests, and payment confirmations that customers want to resolve in the evening

The staffing argument is straightforward: extending coverage through AI costs significantly less than the equivalent live agent hours, and for routine interactions the quality of resolution is comparable. The risk is not in offering the service out of hours; it is in offering it without proper escalation routes for customers who need more than a routine response.

Where should a lender start?

The implementation failures in this space almost always come from starting too broad. The right approach is bounded, measurable, and expandable.

- Pick one high-volume routine call type with clear intent, predictable outcomes, and a clean escalation path. Repayment queries or pre-arrears reminders are the most common first use cases.

- Define the escalation rules before building the bot. What triggers a handoff? How is context passed to the agent? What happens if the customer goes off-script? These decisions shape the whole design.

- Integrate properly. AI voice without a live connection to your loan management system, CRM, and telephony stack produces a poor customer experience and no audit trail. Shallow integration is the most common reason pilots underperform.

- Measure the right things. Freed specialist capacity, time to first contact, arrangement completion rate, and escalation quality. Not just deflection volume.

- Expand only after proving controls. Once the first use case is stable and the escalation model is working, add the next call type. Avoid complaints, disputes, hardship, and complex affordability until the operational foundations are solid.

Do not start with forbearance, repossession, or anything that requires agent discretion. The risk is not the technology; it is deploying it before you have the controls, the integration, and the confidence to expand responsibly.

To explore what a bounded first deployment looks like for your lending operation, speak to us about a cost-modelling session or book a readiness review with our CX and contact centre team.

Frequently asked questions

Which lending calls actually pay off to automate? The strongest first use cases are repayment queries, balance and settlement requests, payment reminders, application status checks, and simple arrangement setup where policy rules are deterministic. Complex affordability, forbearance, vulnerability, complaints, and disputes should remain human-led.

Can AI handle collections and arrears calls? Yes, for routine interactions: pre-arrears outreach, simple promise-to-pay capture, standard arrangement setup, and payment confirmation. Any indication of financial difficulty, distress, vulnerability, or dispute must trigger immediate escalation to a specialist agent with full conversation context passed across.

Where should a lender start with AI voice? Start with one bounded, high-volume routine call type with clear intent and a tested escalation path. Prove the controls, integration, and handoff quality before expanding. Avoid complaints, hardship, and complex forbearance until the operational foundations are solid.

Posts By Topics

- AI (18)

- News (17)

- Unified Communications (17)

- Contact Centre (16)

- Ring Central (13)

- Zoom (13)

- CX (12)

- Events (12)

- Virtual Agent (9)

- Avaya (7)

- Financial Services (7)

- GoToConnect (7)

- Contact Centre Consulting (6)

- Partners (6)

- Case Studies (5)

- Resources (5)

- Unified Communications Solutions (5)

- AI Meeting Assistant (2)

- AI Sales Analytics (2)

- Chatbot (2)

- Conversational Intelligence (2)

- Employee Communications (2)

- Legal (2)

- Microsoft Teams (2)

- Trends (2)

- Video (2)

- AI Companion (1)

- AI Receptionist (1)

- DialPad (1)

- Neurodiversity (1)

- Omnichannel (1)

- Sentiment Analysis (1)

- workvivo (1)