AI Voice Agent Insurance Claims: FNOL Guide 2026

by

Fortay Connect

|

23rd Jun 2026

Posts By Topics

- AI (18)

- News (17)

- Unified Communications (17)

- Contact Centre (16)

- Ring Central (13)

- Zoom (13)

- CX (12)

- Events (12)

- Virtual Agent (9)

- Avaya (7)

- Financial Services (7)

- GoToConnect (7)

- Contact Centre Consulting (6)

- Partners (6)

- Case Studies (5)

- Resources (5)

- Unified Communications Solutions (5)

- AI Meeting Assistant (2)

- AI Sales Analytics (2)

- Chatbot (2)

- Conversational Intelligence (2)

- Employee Communications (2)

- Legal (2)

- Microsoft Teams (2)

- Trends (2)

- Video (2)

- AI Companion (1)

- AI Receptionist (1)

- DialPad (1)

- Neurodiversity (1)

- Omnichannel (1)

- Sentiment Analysis (1)

- workvivo (1)

AI Voice Agent Insurance Claims: FNOL Guide 2026

23 June 2026

Can an AI Voice Agent Handle Insurance Claims Calls? Automating FNOL, IDV and Triage

Yes. An AI voice agent can handle the early stages of an insurance claim call end to end: greeting the caller, verifying their identity, capturing first notification of loss details, classifying severity, creating a claim record, and setting expectations for next steps. For structured, repeatable intake, it is a strong operational fit. For disputed, emotionally charged, or ambiguous cases, fast human handoff is not optional, it is part of the design.

In short: AI voice works for insurance claims intake when three things are in place: reliable identity verification, clean integration into your claims or CRM system, and a governance model that has been reviewed and approved before go-live, not bolted on afterwards.

The sections below walk through exactly what happens on a live FNOL call, where projects break in practice, what the FCA expects, and where a UK insurer, broker, MGA or insurtech should start.

Three things to know before reading on:

- AI voice handles structured early-stage intake well; it does not replace claims adjusters on complex cases

- Identity verification accuracy is the single biggest technical make-or-break factor

- Governance and FCA Consumer Duty compliance should be designed in from day one, not treated as a sign-off step at the end

What Does an AI Voice Agent Actually Do on an FNOL Call?

Most AI-in-insurance content skips this part. Here is what a well-designed AI voice agent actually does from the moment a policyholder calls to report a loss.

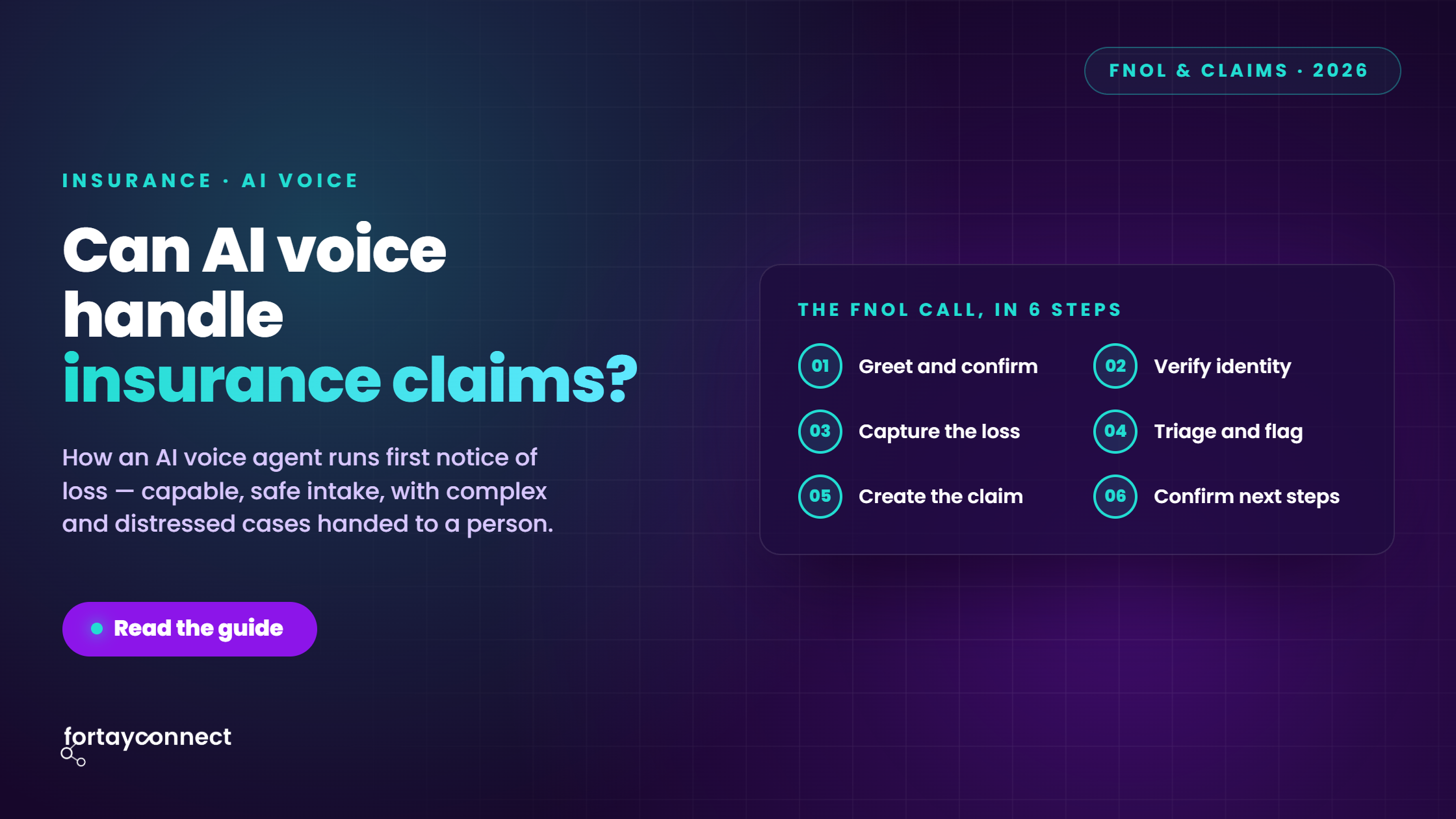

The call sequence, step by step

- Greet and confirm intent. The agent answers immediately, introduces itself as an AI assistant, explains what it can help with, and confirms the caller wants to report a new claim. Transparency here is not optional under FCA Consumer Duty.

- Collect and verify identity. Before capturing any claim data, the agent authenticates the caller using layered checks: policy number, postcode, date of birth, or vehicle registration. More on why this step is critical in the next section.

- Capture incident details. Once verified, the agent collects structured loss information: date and time of the incident, location, parties involved, nature of the damage or injury, and any immediate risk or safety concerns.

- Classify severity and flag escalation triggers. The system assesses the claim against defined thresholds. Injury mentions, fraud indicators, distress signals, policy mismatches, or unclear answers should trigger an immediate warm transfer to a human handler, not a voicemail or callback queue.

- Create the claim record. Structured data captured during the call populates the claims management system or CRM directly. The output is not a transcript sitting in an inbox; it is a usable, time-stamped record with the right fields populated.

- Confirm next steps and close. The agent tells the caller what happens next, provides a claim reference number, confirms any follow-up actions, and ends the call clearly.

What good structured data capture looks like

The value of AI voice intake is only realised if the data coming out is clean and complete. Key fields the agent should capture and pass downstream include:

- Date, time and location of the loss

- Policy reference and policyholder details

- Third-party information where relevant

- Damage or injury indicators and severity markers

- Preferred callback details and consent confirmation

The critical point: average human FNOL handle time sits at around 12.4 minutes. Well-designed AI voice intake can bring structured claims to completion in 5 to 6 minutes, with higher consistency across agents and shifts. The efficiency case is real, but it only holds if the call flow and data outputs are built to claims-system standards from the start.

How Accurate Is Identity Verification, and Why Does It Make or Break This?

IDV is where many voice AI projects stall or fail. If the system cannot reliably verify the caller before the claim is captured, every subsequent step carries risk: data going to the wrong policyholder, fraudulent claims being logged without challenge, or legitimate claimants being blocked and abandoning the call.

The concern is grounded in real deployment experience. Conversational AI setups that were not designed with layered IDV from the outset can perform poorly under real call conditions: background noise, nervous callers, non-standard accents, or callers who do not have their policy number to hand. A single-factor check is rarely sufficient.

What separates strong IDV design from weak IDV design:

|

Factor |

Weak IDV design |

Strong IDV design |

|---|---|---|

|

Verification layers |

Single factor (e.g. name only) |

Two or more factors (policy number + postcode + DOB) |

|

Failure handling |

Call drops or loops |

Clean warm transfer to human with context passed |

|

Confidence threshold |

Binary pass/fail |

Scored confidence with escalation below threshold |

|

Audit trail |

Transcript only |

Timestamped, structured IDV log per call |

|

Fallback options |

None |

One-time passcode, SMS verification, or agent transfer |

|

Vulnerable caller handling |

Not designed in |

Distress signals trigger immediate human handoff |

The accuracy target matters less than how failure is handled. A system that transfers cleanly when IDV confidence is low, passes the context to the human agent, and logs the outcome is operationally safer than one that claims high accuracy but has no fallback path.

The design principle: treat every failed IDV as a handoff opportunity, not a dead end. The caller still gets served; the claim still gets captured; the audit trail is still intact.

Do We Need a Big Team to Run It?

This is the question that kills projects quietly. A voice AI deployment touches telephony, orchestration, compliance, prompt design, claims system integration, and ongoing performance monitoring. When a small internal team is handed a complex platform and expected to own all of that, rollouts stall.

The honest answer is: it depends entirely on the operating model, not the technology.

Platform-led vs advisory-led: the real difference

Platform-led (internal team owns everything):

- Faster initial procurement, slower actual deployment

- Internal team carries full responsibility for integration, compliance, and tuning

- Works well if you have dedicated AI/automation resource and a clear internal owner

- Higher risk of scope creep, delayed governance sign-off, and abandoned pilots

Advisory or managed-service led:

- Slower initial procurement, faster time to a working, compliant deployment

- Implementation burden is shared; change management and governance are built into the process

- Better fit for mid-market insurers, brokers, and MGAs without large transformation teams

- Ongoing performance monitoring and tuning is part of the service, not an afterthought

The practical reality for most UK insurers and brokers: transformation resource is limited. A bounded first deployment, with a clear use case, a defined owner, and external support for integration and governance, is significantly more likely to reach production than a wide-scope internal build.

The goal is a working, compliant deployment in production, not a technically impressive pilot that never scales.

What About Out-of-Hours and Surge Events?

Claims do not follow office hours. A policyholder whose car is stolen at 11pm or whose home floods during a weekend storm expects to report that loss immediately, not leave a voicemail and wait until Monday.

This is one of the strongest operational arguments for AI voice in insurance, and it is specific to the sector in a way that generic contact centre automation is not.

Scenarios where 24/7 AI voice intake delivers clear value:

- Out-of-hours FNOL: Caller reports a loss outside staffed hours; the agent captures the claim, logs it, confirms a reference number, and sets expectations for next-day follow-up

- Weather and mass-loss events: A storm or flood triggers a spike in claims volume that would overwhelm a human team; AI handles structured intake at scale while routing urgent or complex cases to on-call handlers

- Overflow during peak periods: High call volumes during business hours mean callers wait; AI handles initial intake in parallel, reducing abandonment and handle times

- Simple claim status queries: Existing claimants checking progress can be served without consuming handler capacity

The goal is not to automate every judgement call. It is to ensure that every caller is acknowledged, every claim is captured cleanly, and priority cases are routed correctly, regardless of when the call arrives.

Is It Compliant, and How Do We Get It Past Governance?

This is where most deployments slow down or stop entirely. The good news is that AI voice agents can be deployed compliantly under FCA regulation. The harder news is that compliance is the firm's responsibility, not the platform vendor's.

The FCA does not operate a separate AI rulebook. As the FCA's approach to AI makes clear, existing obligations under Consumer Duty, SYSC, and operational resilience apply to AI-handled interactions in exactly the same way they apply to human ones. If an AI voice agent takes a claim from a vulnerable customer without appropriate safeguards, that is a Consumer Duty failure, regardless of whether the interaction was automated.

What the FCA expects in practice

- Consumer Duty outcomes: The interaction must support fair outcomes for customers, including clear communication about what the AI can and cannot do, and an accessible route to a human handler

- Vulnerable customer identification: The system must be designed to detect distress, confusion, or vulnerability signals and escalate immediately

- Recording and retention: Under SYSC 10A, relevant telephone communications must be recorded and retained. This obligation applies to AI-handled calls as it does to human ones

- Audit trail: Every AI-handled claim call should produce a retrievable, time-stamped record of what was said, what was captured, and what action was taken

The internal governance checklist

Before a deployment goes to CIO or IT sign-off, the following should be in place:

- Risk classification documented: use case scope, data handled, customer vulnerability exposure

- Escalation rules defined and tested: what triggers a human handoff and how it happens

- Recording and transcript retention configured and validated

- Bias review completed on IDV logic and triage classification

- Pre-deployment scenario testing under realistic call conditions, including edge cases

- Named senior accountability: who owns the AI agent and reviews its performance

- Vendor governance log: sub-processors, data residency, certifications

The core principle: governance should be designed in from the start, not assembled as a sign-off checklist at the end. Retrofitting compliance is what kills timelines and stalls approvals.

Where Should an Insurer Start?

The most common mistake is trying to automate too much at once. The deployments that reach production fastest start with a single, bounded use case and expand from there.

Start here

- Choose one line of business. Motor FNOL intake is the most common first use case: high volume, structured data, relatively consistent call flow.

- Define escalation thresholds before you build. What triggers a human handoff? Injury, fraud signals, distress, failed IDV, policy ambiguity. Document it before go-live.

- Validate your IDV method. Test it against real call conditions, not a clean demo environment.

- Connect to the claims workflow. The output must populate your claims management system directly; a transcript in an inbox is not a deployment.

- Test governance scenarios. Run the vulnerable customer scenario, the failed IDV scenario, and the out-of-hours surge scenario before you sign off.

- Expand scope after the first use case is stable. Claim status updates, simple notifications, and overflow handling are natural next steps.

Defer these until the first use case is proven

- Disputed liability or coverage interpretation

- Highly complex or multi-party claims

- Calls where vulnerable customer risk is elevated from the outset

For a broader view of platform options that support this kind of deployment, the best AI virtual agent platforms guide for UK mid-market businesses covers the leading options and their relative fit for telephony-led claims intake.

Frequently Asked Questions

What does an AI voice agent do on an FNOL call? It greets the caller, verifies identity, captures structured loss details (date, location, parties, damage indicators), classifies severity, creates a claim record in the claims system, and confirms next steps. Complex, distressed, or ambiguous cases are transferred to a human handler with context passed across.

How accurate is identity verification on an insurance claims call? Accuracy depends on the number of verification layers and how failure is handled. A single-factor check is rarely sufficient. Strong IDV design uses two or more factors, a scored confidence threshold, and a clean warm transfer when confidence is low rather than a binary pass/fail.

Can AI voice agents handle out-of-hours claims and surge events? Yes. This is one of the clearest operational benefits for insurers. AI voice agents operate 24/7, handle unlimited simultaneous calls, and do not require out-of-hours staffing premiums. During weather events or mass-loss incidents, they capture structured intake at scale and route priority cases to on-call handlers.

Ready to Assess Your Claims Intake Use Case?

If you are evaluating AI voice for claims intake and want a clear view of what is feasible, what your governance path looks like, and which platform fits your systems and regulatory environment, a focused readiness session is the right starting point.

We work with insurers, brokers, MGAs and insurtechs across the UK to scope bounded first deployments, assess IDV and integration requirements, and build the governance documentation needed for CIO and IT sign-off.

Book an insurance voice AI readiness assessment to get a structured view of your use case before you commit to a platform or a build.

Posts By Topics

- AI (18)

- News (17)

- Unified Communications (17)

- Contact Centre (16)

- Ring Central (13)

- Zoom (13)

- CX (12)

- Events (12)

- Virtual Agent (9)

- Avaya (7)

- Financial Services (7)

- GoToConnect (7)

- Contact Centre Consulting (6)

- Partners (6)

- Case Studies (5)

- Resources (5)

- Unified Communications Solutions (5)

- AI Meeting Assistant (2)

- AI Sales Analytics (2)

- Chatbot (2)

- Conversational Intelligence (2)

- Employee Communications (2)

- Legal (2)

- Microsoft Teams (2)

- Trends (2)

- Video (2)

- AI Companion (1)

- AI Receptionist (1)

- DialPad (1)

- Neurodiversity (1)

- Omnichannel (1)

- Sentiment Analysis (1)

- workvivo (1)